UAE VAT Update – VAT Public Clarification on the Adjustment on Account of Bad Debt Relief

The Federal Tax Authority (FTA) has released a Public Clarification on the Adjustment on Account of Bad Debt Relief that discusses the conditions that must be met to benefit from the Bad Debt relief scheme.

Conditions for Bad Debt Relief

If the invoice is not paid and a bad debt situation occurs, the supplier of goods or services may proceed with the Bad Debt relief scheme through an adjustment of the output VAT reported to the FTA in the relevant VAT Return if the following four conditions are met:

-

The goods and services should have been supplied, and VAT on the supply should have been charged and accounted for

The FTA clarified that this condition would be satisfied where the supplier has charged VAT on the tax invoice and has also accounted for VAT to the FTA via the relevant VAT Return.

-

Consideration for the supply should have been written off

The second condition requires the supplier of goods or services to write off the whole or part of the consideration for the supply as a bad debt in its accounts.

The FTA clarifies that the bad debt relief can only be taken to the extent of the consideration written off in the accounts. Therefore, if only a part of the consideration is written off, bad debt relief can be taken only to the extent of such written off consideration.

-

More than six months should have passed from the date of supply

Though the invoice is not paid, the supplier of goods or servicesmust wait for six months from the date of supply to avail the benefit from the bad debt adjustment.

The FTA expects that the supplier goods or services should engage with the customer during these six months to recover the debt and collect the outstanding amount.

-

Notification should be sent to the customer stating the consideration for the supply is written off

The fourth condition mandates the supplier of goods or services to notify the contracting party of the amount that has been written off.

In light of the Public Clarification, the FTA expects that the notification must contain at a minimum the following information:

- invoice number and date of the tax invoice which the customer has not paid;

- amount of consideration that the supplier has written off.

The FTA provides neither the specific template of notification nor the method through which a notification should be submitted to the customer.

Therefore, the supplier of the goods or services may decide to include any other information in addition to the above-listed details.

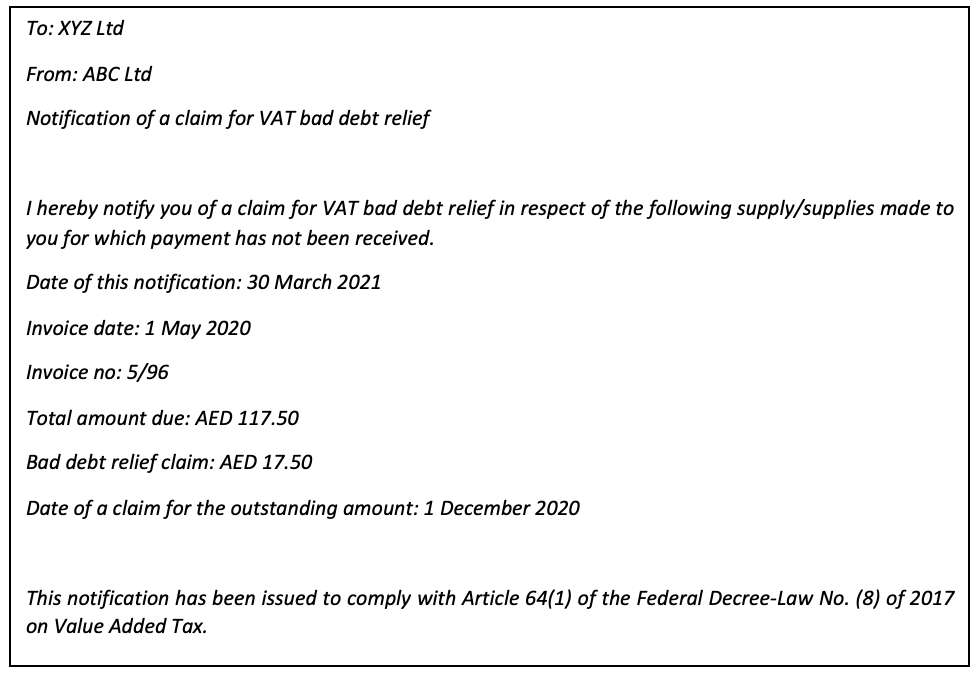

HMRC of the UK, in a guidance issued explaining relief from VAT on bad debts, recommended including the following information in the notification:

- the date of issue of the notification

- the date of your claim for the outstanding amount.

- the date and number of any VAT invoice issued for each supply to your customer, which is included in your claim for the outstanding amount.

- for each relevant supply, the amount which has been written off as a bad debt

Further, the guidance also includes an example of the notification letter, which we have included here for your benefit

Mechanism to claim bad debt relief

Also, the supplier is free to choose the method of notifying the customer. The FTA considers that it would be satisfied when a supplier sends a letter, email, post, or any other similar communication to the customer, stating the amount of consideration written off as long as the evidence of notifying the customer is retained.

Where a VAT registered supplier meets all the conditions as discussed above, it is eligible to claim a bad debt relief in the “Adjustment column” of Box 1 of the VAT Return.

It should be noted that only VAT amount should be reported in the said Box for the relevant Emirate, where applicable, in accordance with the respective Output Tax amount being adjusted.

How can we help?

Rethink as an entity provides VAT advisory, optimization, registration, implementation, compliance, and training services in Bahrain, UAE, KSA, and the GCC.

Our team is here to guide you through the VAT law and regulations and ensure full compliance with the law. Based on our local and international experience, we understand that VAT is a complex tax and would certainly suffer numerous changes in the upcoming years. Rethink’s VAT services are aimed to suit both basic and complex returns for SMEs and larger enterprises

Authors

Keerthi Voodimudi

Senior Manager (Indirect Tax)

Mariia Hordiichuk

Assistant Tax Manager